How the $TREB / System1 deal shows the need for deep pocketed SPAC sponsors

How the $TREB / System1 deal shows the need for deep pocketed SPAC sponsors

As regular readers know, I love pre-deal SPACs trading at or below trust. I love them so much that I’ve mentioned them several times on this site as intriguing opportunities. One of my favorites is Trebia (TREB), which I mentioned as a “quickie” idea in mid-March. They announced a deal with System1 this week, and I thought it might be a good time to revisit that idea and show how the System1 deal highlights the evolving trend in SPACs making deals: if you want to strike a successful deal, your sponsor is almost certainly going to need to have access a truckload of cash outside of the SPAC.

Just to revisit the original TREB idea posted in March: at the time TREB was trading for a slight premium to trust value (~$10.15/share versus ~$10/share in trust). As I write this, TREB is trading for ~$9.92/share. I highlight this past / write-up to drive home a simple point: this is why I love pre-SPAC deals. If you buy them around (or under) trust, your big risks are opportunity cost (plus some small mark to market risk) and your upside is the market falls in love with whatever deal is announced. TREB is helmed by Bill Foley of FNF fame, so there was always a decent chance the market would embrace whatever deal he announced and the stock would go parabolic. Unfortunately, that didn’t happen here — yet — but the way the trade ended up working out still shows a decent risk-return. We ended up taking a ~2% loss in exchange for getting a huge potential upside with the free call option.

So that covers the history of TREB. What I wanted to talk about now is how the TREB / System1 deal’s structure shows what it will take for SPACs to success / get deals done going forward. The only way for most SPACs to “win” a deal is to be the highest bidder in an auction. There are current hundreds of pre-deal SPACs out there chasing the same deals and companies; all of them look pretty much the same (after all, a SPAC is a pure cash shell and one cash shell is basically the same as the next) and a SPAC’s management team will lose millions of dollars in promote if they cannot successfully find a deal. That puts SPACs in something of a Catch-22: they need to be the highest bidder to win an auction and present a merger to their shareholders, but if they bid too high, their shareholders will believe they overpaid and rush en masse for the exits (i.e redeem their shares). If too many shareholders redeem, then the SPAC won’t deliver any cash to the target company and the deal will fail, and the target company will have gone through the headache and expense of trying to merge into a SPAC for zero payoff. That’s an awful outcome for every party involved.

That’s why I’ve been arguing that the best place to invest in SPACs is with sponsors who have deep pockets and a proprietary deal flow. For example, one of my favorite SPACs is Liberty Media’s LMACA. Liberty has the best relationships in all of media and telecom, so they can get access to creative / proprietary deals deals no one else can. In addition, Liberty has access to billions of dollars in funding, both directly at the corporate level and from John Malone stans who would be eager to throw money at his next deal. That’s a powerful combo. Liberty will eventually be able to identify and consummate a merger deal that probably wouldn’t be available to any other SPAC, and when it does, it can guarantee the target some minimum cash level because Liberty and its friends will be able to backstop it all. Few others SPACs can offer that combo of cash certainty and proprietary deals.

TREB checks many of the same boxes that LMACA does. Foley has a great track record and deep pockets, and given his decades of deal-making he has contacts and access to deals that most SPACs won’t see much less get anywhere near.

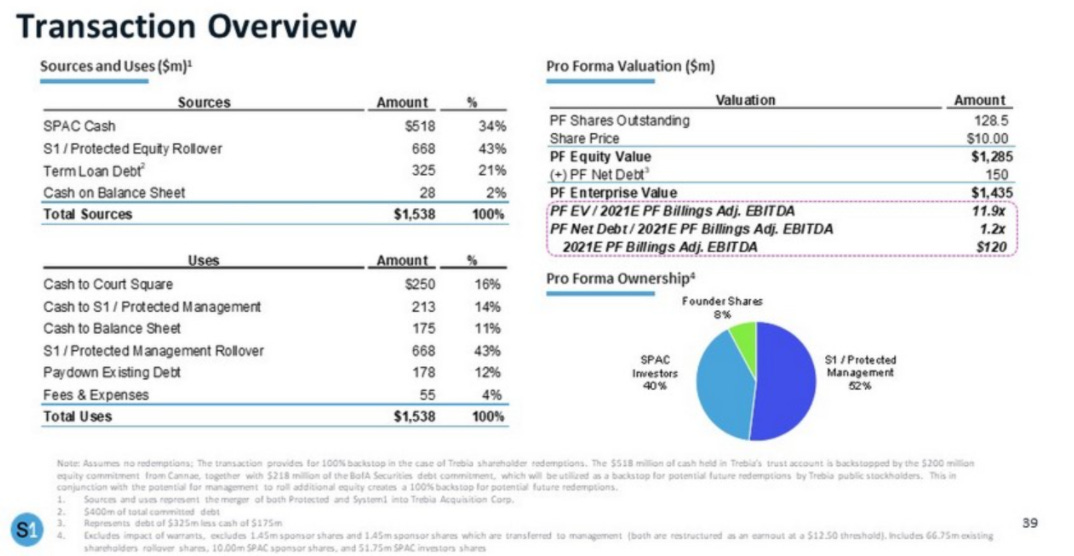

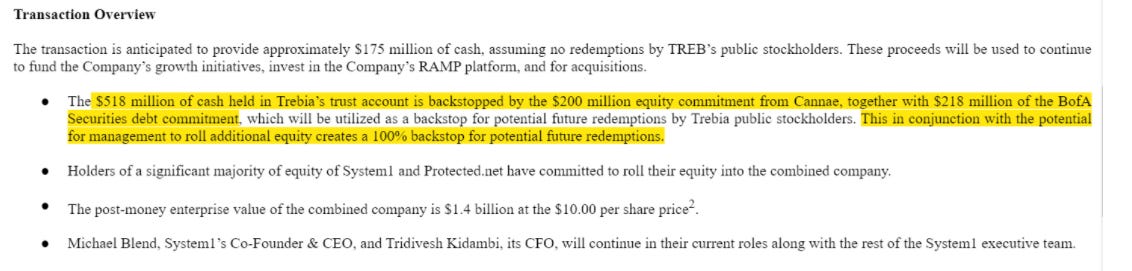

I think you can see how these characteristics positively influenced the Trebia / System1 deal. Trebia had ~$517.5m in trust and another $75m in a forward commitment from Cannae (CNNE), one Foley’s controlled companies that was also part of the sponsor group. In total, if no investors redeemed, Trebia would deliver just under $600m in cash to its target. Of course, calculating based on nobody pulling their money is a big assumption. Redemptions have been running pretty high in recent deals as the SPAC universe cools from its February peak. To pick a somewhat extreme example, GIX recently completed its UPH deal. The company had ~17.25m shares outstanding, and over half (~9.4m) redeemed when the tie-up was signed last month. (The deal went through despite the exodus, thanks to some shenanigans with the backstop.)

That redemption risk makes it difficult for sponsors and companies to determine a fixed point around which to negotiate. How does Trebia go to a company and say, “We’d like to do a merger. The deal might deliver $75m to you, or it might deliver ~$600m, depending on how excited investors get about it.” It’s tough to come to an agreement out of that kind of chaos.

The solution is to have outside capital willing to backstop the deal or cover redemptions. A good example of this is the recent TBA / IronSource tie-up. The SPAC has $1B in trust, and they struck a deal that had $1.3B in PIPE. On top of that, Thoma Bravo, the sponsor, agreed to purchase another $250m of shares to cover redemptions if investors redeemed more than $150m. That’s a powerful combo: it narrows the range of cash that IronSource would receive and guaranteed a minimum cash level for IronSource. It also was a powerful signal from the sponsor: they invested $300m into the PIPE and agreed to cover another $250m of redemption. Money talks, and in this case TBA was signaling to shareholders that they believed in the IronSource deal and were willing to put their money where their mouth was / alongside SPAC shareholders.

WPF, another Foley SPAC, dealt with that issue in a similar way. The SPAC had just over $1B in trust, and their merger agreement included ~$1.55B in PIPE investment and $300m from its forward purchase agreement. Even with that, ~20% of their SPAC shares redeemed, so WPF decided to extend the window for shareholders to withdraw their redemptions and have their sponsors cover a quarter of the shares that redeemed.

Real companies want some deal certainty when negotiating a big transaction like a deal SPAC, so the fact that deeper-pocketed sponsors can put in big PIPEs and backstop deals is a huge leg up in negotiations.

What drew my attention to the TREB / System1 deal is the structure. Trebia is using debt to backstop part of the redemption guarantee. I’m not sure I’ve seen that before. In fact, the whole structure is pretty unique.

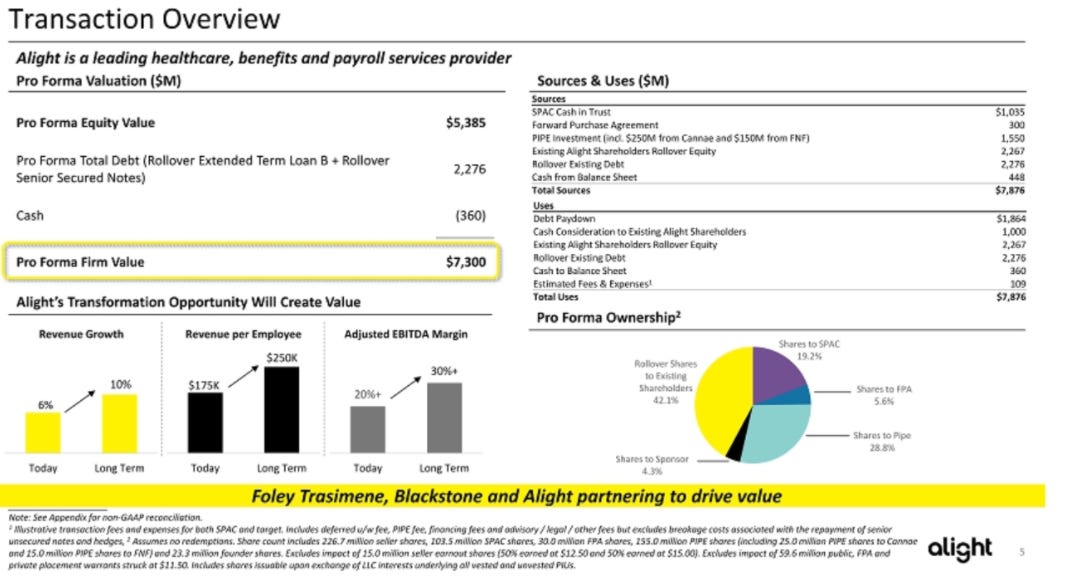

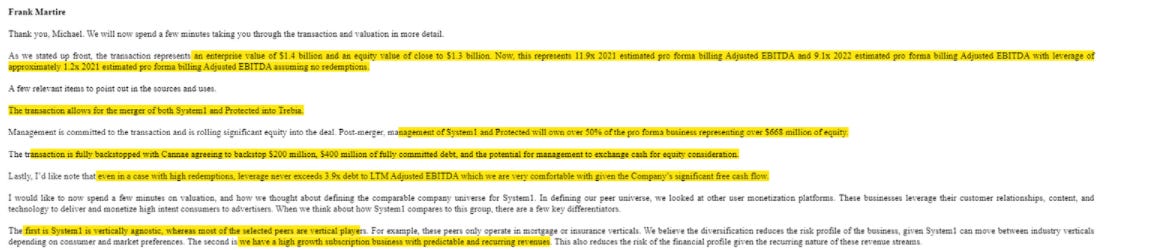

Again, TREB has ~$518m in trust and had a forward purchase agreement from CNNE for another $75m. As part of the System1 deal, TREB and CNNE are cancelling the forward purchase agreement. Instead, CNNE will backstop the first $200m of redemptions. TREB has also lined up a $218m debt commitment from BoA to cover any redemptions above the $200m CNNE backstop level. That covers $418m of the $518m CNNE has in trust. On top of those backstops, System1’s management team has agreed to roll $100m of equity in place of cashing out if redemptions exceed $418m. In other words, TREB has managed to structure a deal that delivers a baseline level of cash to System1 even if every minority TREB shareholder redeems. (You can quibble with this because once redemptions top $200m, System1’s debt goes up, and I’m not sure management’s promised equity roll really changes the deal dynamics. Still, it’s a structure that guarantees access to hundreds of million in cash no matter what shareholders do) (clip below from the merger announcement)

I suspect we’re going to see more deals structured like TREB’s going forward. Companies will quickly realize that SPAC negotiations with shaky sponsors and without big equity backstops simply aren’t worth pursuing. The redemption levels are too high, which means the cash delivered is too small, and nobody wants to get dragged through the heartbreak of months of deal calls / SEC filings / dealing with lawyers only to see a deal that delivers almost nothing in the end because all the shareholders redeem. Look for waves of smaller SPACs with subpar sponsors to fail to find deals and eventually liquidate, while larger sponsors with deep pockets will come out better because they’ll be able to structure deals in innovative ways that guarantee minimum cash levels to the companies they’re merging with. That’ll give them advantages in negotiations and help push deals over the finish line. (clip below from the merger call)

My core takeaways: As the hangover following the SPACmania from earlier this year continues, money will talk. Smaller sponsors will struggle to find deals (or, having found a deal, struggle to get their shareholders to vote it through, while SPACs with strong sponsor group with have an increasing edge in negotiating with companies and delivering deals going forward. That edge presents opportunity: plenty of pre-deal SPACs with good sponsors are trading below trust right now, and, while not all of them will work out, a few of them will find deals that the market ends up loving and trading significantly through trust.